Leave your details and we'll call you back

We can call you at a time that suits you.

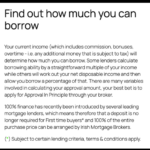

First of all, a broker works with numerous banks or other lending organizations and can locate the best prices and conditions for you. Consider a broker as the intermediary between you and possible lenders and banking companies. A bank is, of course, an institution-specific direct lender. Many householders are looking for the best rates for loans. From 8 to 30 years, you’ll be stuck with your mortgage. Therefore you want a monthly payment that’s convenient to you.

There are a few benefits to utilizing a mortgage broker, such as access to an extensive range of lenders; because brokers have access to a large number of direct lenders, they can shop and match your circumstances. They are like a personal tour guide who selects the finest airlines, hotels, and car rental businesses to get the most incredible bargain for you. You have your back, and they’re going to work together to make it work. A broker also saves you long-term time. As only one application must be submitted in full instead of only one application for each bank or lender alone, the relief might be enormous. Right now, anyhow, you probably have enough on your plate! You will then proceed with your choices, including the rates, points (if applicable), and closing expenses, once you’ve applied to your broker. In other words, they simplify the comparison.

Although a broker cannot guarantee that it is cheaper than a private lender, let’s be honest: most consumers do not have the time (or the proper resources) to get away and prefer all lenders and rates. It might be time-consuming to approach your bank, and even then, you have only one comparison. It will be far cheaper to engage with a broker than take your risks and go straight in most circumstances. Be careful, however, because couriers have access to wholesale loan rates from lenders, which generally means lower costs to begin with — every rise of the expenses due to the charge for your broker typically ends up being washed out.

After all, you and your interests are represented by your broker, rather than a bank – in which you may be a number (or commission) for them. Thus, it would help if you planned to offer your broker a great deal of information about your unique demands and position beforehand. Do you have questions about the process? Your broker will help you discover answers and provide you with informed advice in your best interest. Is the issue complicated? A skilled mortgage broker will identify new solutions for you. In addition, your broker can assist and prevent you from lending from unscrupulous lenders. For example, you will frequently find fishy payment conditions in the contract when you notice a rate that looks too good to true. And this might be a very costly error over the life of a loan. Finally, especially as a new homeowner, you will probably learn a lot about mortgages and all their vocabulary—it may be a lot! Your broker will assist you in grasping the offerings on the table in detail.

Naturally, there may be scenarios when you do not fit with dealing with a mortgage broker. Here are some things to remember. First, brokers usually have additional charges Brokers generally demand a fee in return for their services and contacts. Sometimes, the loan charge is paid for by the lender, and in some instances, it is added to your closing fees —so you want to look into this and understand the conditions before signing anything. Second, there is no assurance of the best deal from your broker. You can be quoted higher rates or be more likely to score a fantastic deal if you have built a relationship with a bank (for example, if you’ve been a longtime member with current accounts or have other forms of loans with them). Loan officers also have a little more flexibility at such organizations. They can provide unique discounts, create exceptions or even waive some charges to typical policies. Again, when you decide and evaluate your alternatives, you’ll want to take this into account.